Medicare Advantage

vs Medigap

Broad Overview of Medicare Advantage vs. Medigap

Medicare Advantage vs. Medigap is perhaps the number one question we get daily. This is because the Medicare Advantage carriers do a great deal of marketing to seniors because MA plans are highly lucrative for them. What is Medigap? Medigap plans also go by the name Medicare Supplements.

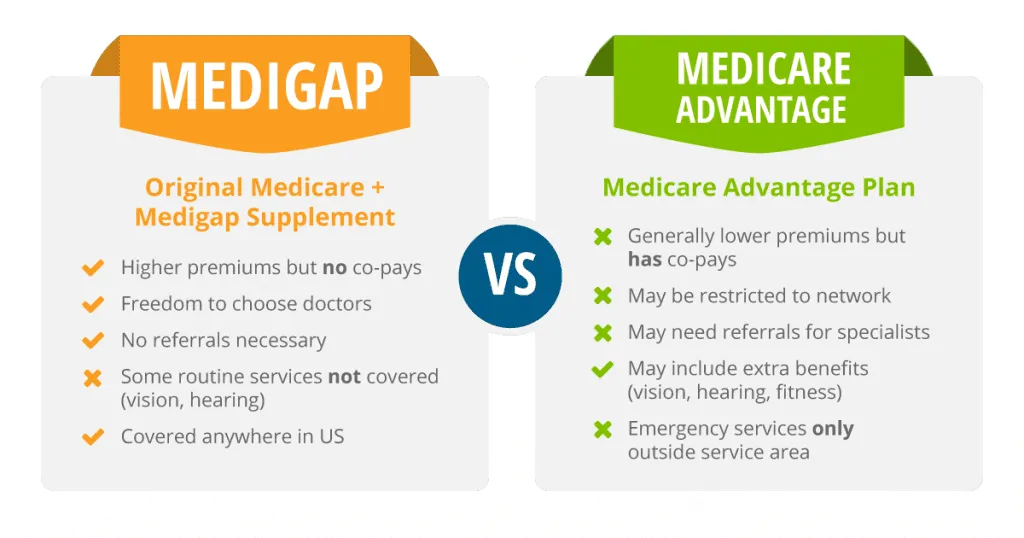

In a nutshell, Medigap plans are the Cadillac option while Medicare Advantage plans are the opposite. Medicare Advantage plans, also known as MA or MAPD plans will often have a zero dollar monthly premium but cost more when you use them.

Medicare Advantage plans will have copays for doctor visits, hospital visits, X-rays, labs, etc. In contrast, a Medigap Plan F has a monthly premium but pays for all covered expenses incurred. Medigap Plan F has a $0 deductible and 100% coverage for everything I just mentioned. Plan G has a $233 deductible and 100% coverage for everything above. In addition, the Medigap plan also has no network, meaning you can visit any provider who accepts Medicare. With a Medicare Advantage Plan, you must stay within that plan’s network. While many are HMOs, PPO’s have become more available in recent years. Medigap plans do not cover prescription medications purchased separately, as explained below.

Detailed Overview of Medicare Advantage vs. Medigap

Price

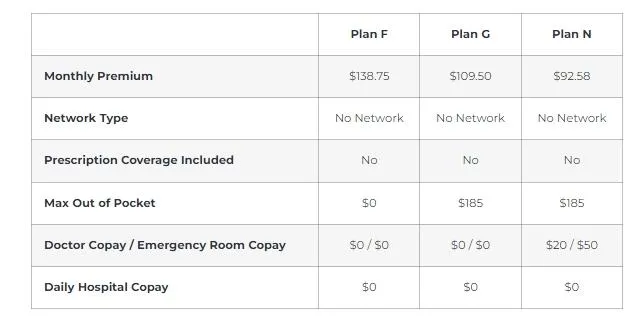

Medicare Advantage plans usually have a zero monthly premium. However, some of the more comprehensive plans can have a premium. An example of this is below. Medigap premiums vary based on the Plan letter, age, zip code, etc. We’ll pick a zipcode at random; 30303 in Atlanta, Georgia. We’ll use a 65-year-old female who does not use tobacco. The lowest cost Plan F as of this writing is $138.75 monthly. The lowest cost plan G is $109.50 and the lowest cost Plan N is $92.58.

On the price front, it’s important to note that regardless of which option you have, you must continue to pay your Part A and Part B premium. For most people, Part A is at no cost as you paid it during your working years. For those wondering about Part B costs. Good question, however, we do have a separate article on the topic because it’s based on income and can be complicated. See: How much is Medicare Part B

Network

As stated above. Medicare Advantage plans have networks where Medigap plans do not. With a Medigap plan, you may visit any provider you wish as long as they take Medicare. This is very easy to do via medicare.gov/physiciancompare/

With Medicare Advantage, you could be required to use your Medicare Advantage plan’s network of providers. This may be a narrow network, local HMO, or a broader network PPO. Many PPO Medicare Advantage Plans now offer out-of-network coverage as well. Most HMOs will require you to visit your primary care provider for a referral to a specialist. One of the chief complaints we receive in our office about Medicare Advantage plans is a lack of providers and/or doctors leaving the networks.

Per day of each benefit period.

Ability to Purchase

This is a very big difference between the 2. Medicare Advantage plans can be purchased when you turn 65, and every year thereafter during AEP (10/15 – 12/07 annually). There are no medical questions, and as long as you are not in end-stage renal failure, you can get a plan.

With Medigap plans, you get one open enrollment in your lifetime. That period of time is the first 6 months after you turn 65 years old AND are enrolled in Medicare Part B. For most people, this occurs at age 65. For those who work past 65, it happens when they retire. During this 6-month open enrollment period you cannot be declined for a Medigap plan, nor can they ask health questions. Your acceptance is guaranteed at the best rate available. Once this 6-month period ends, unless you have a qualifying life event, you will be required to answer health questions if you ever want to change your Medigap plan. While this isn’t the end of the world, as seniors over 65 change carriers every day, it can be a roadblock in moving from Medicare Advantage to Medigap in later years..

Stability

Medicare Advantage plans can change every calendar year. Medicare Advantage changes can include doctor networks, copays, out-of-pocket maximums, drug formularies, etc. Medigap plans are standardized by the government and do not change from year to year

Part D Prescription Coverage

Medicare Advantage plans can come in MA or MAPD form. The MA is an acronym for Medicare Advantage and the PD is an acronym for Part D which is the part of Medicare that handles prescription drug coverage. MAPD plans have the Part D coverage built-in, so you only need 1 plan. Medigap plans do not have Part D built-in, so this needs to be purchased separately. The average cost for 2022 is $31.47 per month for Part D coverage. This would be on top of your Medigap premium.

Chemotherapy

While this isn’t something most people think of, it is a key difference when it comes to comparing Medicare Advantage vs Medigap.

Most Medicare Advantage plans cover chemotherapy at 80%, leaving you with the 20% coinsurance to pay until your annual maximum is paid. This out-of-pocket maximum can be up to $8,000 annually.

If you are the owner of a Medigap plan, then this is a huge difference. With chemo or anything else for that matter, you are responsible only for your deductibles and copays. With Plan F – $0 deductible. On Plan G – $233 deductible. Plan N – $233 deductible and $20 office visit copay / $50 hospital copay.

Extra Benefits

Medicare Advantage plans very much want your business, so as of recent years they have been including many extra benefits to try and attract seniors who would otherwise choose Medigap plans. MA plans will sometimes include hearing benefits, dental and vision benefits, and SilverSneakers. While some Medigap plans will offer SilverSneakers, most of the other benefits are not included with Medigap plans and would need to be purchased separately.

Medicare Advantage vs Medigap Benefits Comparison

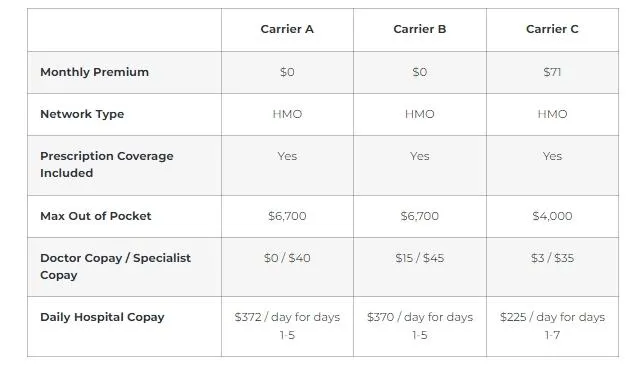

Below is a comparison of 3 Medicare Advantage plans in Atlanta, Georgia 30303. Because of the intense regulation of MA plans and the overwhelming scrutiny they put on agents and brokers, I’m omitting the names of the carriers. I can assure you that these are 3 mainstream, name-brand insurance companies that you’ve heard of. These are obviously not detailed overviews, however, these encompass the biggest components of the plans that consumers tend to focus on.

Medicare Advantage Benefits Comparison

Below is a comparison of 3 Medigap plans. As a reminder from above, we used rates for a 65-year-old female, who does not use tobacco in Atlanta, Georgia 30303.

Medigap Plan F, G, and N Benefits Comparison

Prescription Coverage Continued

In the Medicare world, prescription drug coverage is compared for an insured by inputting each of the drugs they take on a regular basis. Because of this, it wouldn’t be very helpful to draw a comparison between plans because the purpose of this article is Medicare Advantage vs Medigap.

The important takeaway from this article is that if you have Medigap, then you also need to buy Part D, and knowing the average monthly premium of $31.47 (for 2022) will help you in your financial comparisons of the two.

Medicare Advantage vs Medigap – Which Do I Recommend? I’ll keep this simple and brief.

I tell most clients “If you can afford a Medigap plan, buy a Medigap plan”. If at some point in the future, the premium becomes a burden, you can ALWAYS switch to Medicare Advantage, but the same isn’t always true in reverse. Medigap plans provide you with the most flexibility and most comprehensive benefits. If the premium is a concern, then consider Medicare Advantage. The MA system is phenomenal and as long as you completely understand the plan you’re buying, you can’t make a bad decision.

As always, if you have any questions regarding Medicare Advantage vs Medigap or anything else for that matter, give us a call at (770) -790-4571

Healthcare Marketplace For America specializes in affordable health insurance solutions for seniors, individuals, and business owners.

1700 Northside Drive Atlanta, GA 30318, United States

+1 470-876-7490

Health Insurance

Open Enrollment 2024

Individual/ Family Health Insurance

Short-term Health Insurance

IFP Health Plan Guide

NCD Dental & Vision

Open Enrollment 2024

Open Enrollment 2024

Open Enrollment 2024

Open Enrollment 2024

Medicare

What is Medicare?

What is Medigap?

Medicare Advantage vs. Medigap

Medicare Costs for 2024

Medicare Part A

Medicare Part B

Medicare Part C

Medicare Part D

Health Insurance

About Us

Meet the Team

Contact Us

Licensing Information

Privacy Policy

Connect with Us

@hmforamerica

@hmforamerica

©Healthcare Marketplace For America 2024 All rights reserved. Privacy Policy